LNG in World Markets: US Export Projects in Pole Position for FIDs

US Export Projects in Pole Position for FIDs

This current feature was extracted from the latest edition of Poten’s LNG in World Markets, a monthly service published on January 31, 2023.

Progress on sales and purchase agreements (SPA), engineering, procurement and construction contracts and major equipment purchases show that three US LNG export projects are in the pole position to reach final investment decisions (FID) this year. Mostly indexed to the gas benchmark Henry Hub (HH), US LNG remains an attractive option for buyers seeking both flexible cargo destinations and the ability to avoid high Brent crude-linked prices, amid limited options after western sanctions slowed down construction of Russian liquefaction projects.

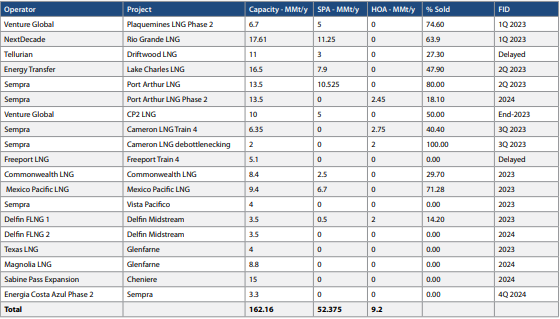

Phase one of Sempra’s Port Arthur LNG in Texas, Train 1 through Train 3 of NextDecade’s Rio Grande LNG in Texas and phase two of Venture Global LNG’s Plaquemines LNG in Louisiana are all poised to reach FID this year. Combined, the three projects will add around 38 MMt/y to constrained global supplies with initial production beginning in 2026 or 2027.

Outside the US, only TotalEnergies-led Papua LNG is looking to take FID this year, although a few floating liquefaction (FLNG) projects are wild cards for final sanction in 2023.

Global producers reached FID on only 23.3 MMt/y of LNG supply last year. That came from two US projects – phase one of Venture Global’s Plaquemines LNG and Cheniere Energy’s Corpus Christi Stage 3, as many other US sponsors missed their 2022 FID targets.

Port Arthur LNG first up

After selling 80% of phase one of Port Arthur’s nameplate capacity, Sempra tops the FID list this year. Sempra-owned Port Arthur LNG signed five sales and purchase agreements (SPAs), mostly with European buyers and is currently discussing project finance with banks.

In late January, the company converted its heads of agreement (HOA) with Poland’s PKN Orlen to an SPA at 115% of the HH gas price plus a $2.08/MMBtu liquefication fee. The HOA was originally signed by Poland’s PGNiG but PKN Orlen inked the deal following its acquisition of PGNiG. The deal is the last one that Sempra needed to convert to an SPA after finalizing deals with ConocoPhillips, Ineos, Engie and RWE.

ConocoPhillips is an equity partner and the largest offtaker with 5 MMt/y of the plant’s volumes. Pricing for the equity offtake is $2.05/MMBtu plus 115% of H. Port Arthur LNG’s other customers will be paying 115% of HH plus liquefaction fees ranging from $2.08 to $2.30/MMBtu.

Sempra is approaching the Feb. 8, 2023, deadline to issue a full notice to proceed to engineering, procurement and construction (EPC) contractor Bechtel to keep the $10.5 billion price to build its proposed 13.5-MMt/y phase one of the Port Arthur LNG export terminal in Texas. It has already issued Bechtel a limited notice to proceed with some construction activities. If Bechtel takes FID after Feb. 8 but before May 8 the EPC contract price goes up by $149.4 million. If a full notice to proceed is not issued by May 8, Sempra and Bechtel must agree to a further EPC price adjustment.

NextDecade to sign deal with TotalEnergies

NextDecade is expected to announce shortly that it has signed its final and largest SPA of around 4 MMt/y with TotalEnergies. The French oil major will inject equity into Rio Grande LNG, giving it the final push towards its February FID target and taking its overall contracted capacity to 86% from 64%. NextDecade, like Sempra, is holding discussions with banks to secure project finance.

The US project developer announced an SPA with Japanese trading arm Itochu this month for 1 MMt/y for 15 years and China’s ENN Natural Gas in December for an additional 500,000 t/y for 20 years. Pricing for the deal with Itochu and ENN are at 115% of HH plus $2.20-2.25/MMBtu and 111% of HH plus $2.10-2.15/MMBtu, respectively. Itochu had originally sought to buy 700,000 t/y but raised supply to 1 MMt/y to qualify as a foundation buyer. ENN will lift the additional 500,000 t/y from Rio Grande LNG Train 3 while Itochu will have access to supply from Train 2 and Train 3. These deals and an earlier SPA with Spain’s Galp put binding contracts at 11.25 MMt/y.

NextDecade is also using Bechtel as an EPC contractor for the 27-MMt/y Rio Grande LNG project. Bechtel holds a pair of contracts worth a combined $11.2 billion to build 17.6-MMt/y phase one of capacity across Rio Grande’s first three trains.

Bechtel has already started with some early site work after NextDecade issued a limited notice to proceed in October. Aerial images and Federal Energy Regulatory Commission (FERC) filings show continuing work at the Rio Grande LNG site. NextDecade is targeting FID in March.

Now operating under a clause where NextDecade issues a notice to proceed between Dec. 15 and March 15, Bechtel and NextDecade will have to negotiate a change order to the contract. Sources familiar with the matter said that could drive up the EPC contract price by $1 to $3 million for each day of delay, adding between $90 million to $240 million to the total cost of the project.

If NextDecade issues a notice to proceed after March 15, Bechtel will draft a revised proposal for work and the contract price. Bechtel can terminate the contract without any liability if NextDecade fails to issue a notice to proceed before July 31, 2024.

Plaquemines LNG phase 2 sells 5 MMt/y

Venture Global LNG is also likely to reach FID this quarter for the 6.7-MMt/y second phase of its Plaquemines LNG export terminal in Louisiana. The company has secured 5 MMt/y of contracts for Plaquemines LNG phase two after making FID and obtaining $13.2 billion in project finance for phase one in May last year.

Construction is already underway for phase one of the project and recent equipment orders suggest FID for phase two is imminent. For phase two Venture Global has already ordered 12 cold box systems worth $91.8 million from Chart Industries, power generation equipment and 12 modularized compression trains from Baker Hughes.

More projects target 2023 FID

Other LNG export projects that also have a good chance of reaching FID this year are Venture Global’s CP2 LNG, Sempra’s Train 4 expansion, Mexico Pacific Ltd. (MPL) and Delfin FLNG.

Venture Global has contracted 5 MMt/y from its 10-MMt/y CP2 LNG project. If its deal with Jera goes through, it would bring contracted capacity to 7 MMt/y. However, Venture Global is awaiting FERC approval for CP2 LNG. FERC suspended an environmental review timeline for the project in July because the developer did not provide all the requested information.

FERC plans to issue the final environmental impact statement (EIS) draft by January 2023. The issue of notice of availability of the EIS is expected on July 28 and there is a 90-day federal authorization decision deadline on Oct. 26, following the EIS. This means that Venture Global will only be able to take FID for CP2 LNG towards year-end at the earliest. After quietly selling half of CP2 LNG’s capacity, Venture Global is starting to market volumes for its Delta LNG project.

Sempra is close to completing its front-end engineering design for 6.35-MMt/y Cameron Train 4. Sempra has asked for EPC bids by the end of March and will select a contractor by September. It aims to take FID by 4Q 2023. Sempra plans to lift 3 MMt/y from the project and has already committed 2 MMt/y to PKN Orlen and 750,000 t/y to Williams through HOAs. Cameron shareholders TotalEnergies, Mitsui and Mitsubishi will offtake slightly less than 1 MMt/y each from the project. Completion of the project is expected in 2027. Shareholders project initial breakeven costs at mid-to-high$2s/MMBtu on an FOB basis.

MPL has signed a 2 MMt/y long-term sale and purchase agreement with a portfolio player, after signing deals for 2 MMt/y with China’s Guangzhou Development Corp. and 2.7 MMt/y with Shell. Exxon is understood to have conducted due diligence on the project since late last year. This leaves MPL with only one final SPA to secure with the foundation buyer before taking FID on its 9.4-MMt/y Saguaro Energia project. MPL is offering buyers the option to choose between HH or Waha hub gas prices every five years. The initial index can be either Waha or HH.

Delfin makes progress on FLNG project

Delfin Midstream is advancing commercial discussions and financing for its first 3.5-MMt/y floating LNG vessel with a target of reaching a final investment decision in 2Q 2023. The company expects to announce another SPA in February. It is in final SPA talks with Hartree Partners for less than 1 MMt/y. Delfin Midstream signed a 1-MMt/y HOA for tolling capacity with Devon Energy for the first vessel, plus a 1-MMt/y option for the subsequent vessel. Pricing is at 115% of HH plus $2.20/MMBtu.

Delfin has also signed an HOA with Centrica for 1 MMt/y for 15 years and a SPA with Vitol for 500,000 t/y for 15 years. The Vitol contract includes equity investment structures where 50% of the price is tied to upside sharing and the remaining 50% is tied to a netback of JKM or TTF benchmarks plus mid-$1s/MMBtu. The company expects to flip its HOAs with Devon and Centrica in February or March. It remains to be seen whether such price structures would be accepted by banks for project finance.

Delfin’s first FLNG vessel will require a capital raise of $2.5 billion. Delfin has secured a yard slot with Samsung Heavy Industries for the first vessel. The company expects to make an equity investment announcement in March or April, most likely with a single equity partner for the whole sum. It plans to have more equity than debt under its equity/debt ratio.

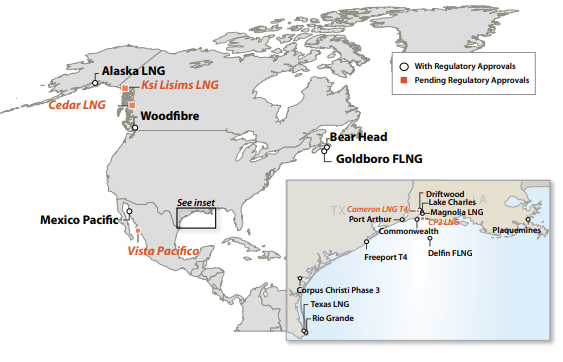

North American Projects

SUBSCRIBE TO POTEN'S LNG IN WORLD MARKETS

Industry participants rely on Poten’s LNG in World Markets business intelligence service for the best information to drive business success. To activate your subscription or learn more, connect with us today: [email protected]